For all the opportunities that the globalized economy has brought, US citizens can run into trouble when it comes to the complexities of international taxation and the risk of being taxed twice on the same income.

The Foreign Tax Credit solves this by offering a dollar-for-dollar reduction in US tax obligations for those who have already paid their dues to foreign governments. What makes this provision particularly valuable, however, is its treatment of excess credits when foreign tax payments exceed US tax liability. Instead of vanishing, these credits can be preserved.

In this article, we’ll examine the Foreign Tax Credit carryover system, the common pitfalls, and how Harness can help keep your international tax planning efficient and effective.

Key takeaways

- The Foreign Tax Credit helps prevent double taxation by allowing US taxpayers to extend their use for up to a decade.

- Excess credits require careful tracking and strategic planning, as they need to be categorized by income type and applied according to strict IRS guidelines.

- Common pitfalls include misapplying credits, missing filing deadlines, and improper documentation. With professional guidance, however, this valuable provision can significantly reduce your global tax burden.

Table of Contents

- What is a foreign tax credit carryover?

- Carryforward vs. carryback options

- Qualifying for the foreign tax credit carryover

- Calculating your FTC carryover amount

- Documentation and filing requirements

- Common traps and pitfalls to avoid

- Strategies to maximize FTC benefits

- How Harness can help

What is a foreign tax credit carryover?

The Foreign Tax Credit Carryover is an IRS provision that takes into account the fact that international tax situations rarely align perfectly within a single tax year. The provision creates a 10-year window for using excess credits, with an additional option to reach back into the previous tax year.

A U.S. citizen working in Germany, for example, will be faced with tax rates that often exceed US levels. Without the carryover provision, the excess taxes paid would simply disappear—a financial loss that could amount to many thousands of dollars.

Within the carryover system, the IRS maintains strict separation between different types of income. Your salary, consulting fees, and other general income occupy one category, while investment returns, rental income, and similar passive sources belong in another. Each category maintains its own carryover balance, requiring separate tracking and strategic planning.

Year-to-year income fluctuations, common among international professionals, can make these carryovers particularly valuable. A high-tax year might generate credits that prove useful during leaner periods or when transitioning between countries with different tax structures.

Carryforward vs. carryback options

The choice between carrying credits forward or backward provides major flexibility in tax planning. Looking ahead, the 10-year carryforward window offers profound tax opportunities. An expat anticipating a future return to the U.S. might strategically preserve foreign tax credits for years when they will face higher U.S. tax exposure.

Looking backward, the carryback option can unlock immediate value. To generate a potential refund check, one can apply excess credits to the previous year’s tax return instead of waiting for future opportunities to use those credits.

Efficient tax planning means carefully evaluating these options. A pending move to a lower-tax jurisdiction might make immediate use of credits more attractive. Conversely, possible career advancements or investment gains could make preserving credits for future years the wiser choice.

Qualifying for the foreign tax credit carryover

To claim a Foreign Tax Carryover, you need to file Form 1116. This is an important choice (often made in your first year working abroad) as simply taking the foreign taxes as an itemized deduction permanently eliminates any opportunity to carry forward excess credits. This single decision can impact your tax strategy for up to a decade.

That said, not all foreign taxes qualify for these credits. The IRS seeks a rough equivalence to US income taxes, generally accepting levies that target income rather than consumption or property. A German income tax qualifies, for example, but a French wealth tax doesn’t.

Tax planning is also affected by political and policy limitations. The IRS maintains a specific list of countries where tax payments do not qualify for credits, often due to U.S. diplomatic or economic concerns. What’s more, a core policy rule aims to prevent double benefits: if you choose to shelter foreign-earned income using the Foreign Earned Income Exclusion, the taxes paid on that excluded income cannot be claimed as a Foreign Tax Credit.

Proper documentation is, therefore, essential to shield against any future IRS scrutiny. Beyond proving that foreign taxes were legally imposed, you must demonstrate actual payment. Bank records, foreign tax returns, and payment receipts form the foundation of a meaningful paper trail.

Calculating your FTC carryover amount

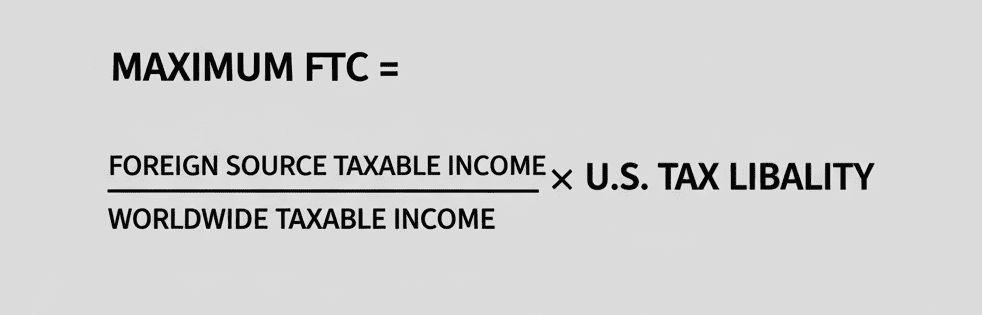

A precise mathematical formula governs your maximum allowable Foreign Tax Credit.

When calculating your credit limit for the year, you divide your foreign income by your worldwide income and multiply by your US tax liability. However, this seemingly straightforward calculation often reveals surprising complexities.

When foreign taxes exceed this limit, the difference becomes your potential carryover. A London-based financial analyst paying UK taxes at 45% might find that the US tax liability covers only a portion of these payments, creating substantial carryover opportunities.

Currency conversion adds another layer of difficulty. The IRS provides official exchange rates, with consistency across tax years crucial to the process. Using different rate sources, methodologies, or calculations can trigger IRS scrutiny and potentially invalidate claimed credits.

The Foreign Tax Credit Carryover Worksheet offers a step-by-step guide to these calculations. This document, tucked within the Form 1116 instructions, helps track credits by year and category. As useful as this may be, many taxpayers find that professional assistance is necessary, particularly when dealing with multiple countries or income streams, as each additional variable multiplies the computational complexity.

Documentation and filing requirements

As mentioned, Form 1116 is the basis of Foreign Tax Credit claims. You need to file a separate form for each income category (or “basket”), which creates the foundation for tracking both current credits and carryovers.

The Foreign Tax Credit Carryover Worksheet records where excess credits originated, how they have been used, and what remains available. This systematic log is essential during any IRS examination, as it serves as your first line of defense.

Systematic record-keeping is crucial throughout the entire filing process. The special 10-year statute of limitations for FTC claims means you need to retain all supporting documentation (foreign tax returns, payment receipts, etc.) for at least 11 to 13 years.

A core rule for the Foreign Tax Credit is that current year taxes take precedence over carryovers. Only once foreign taxes paid in the current tax year have been applied against the annual FTC limit, can carryover credits from prior years be used. Importantly, these carryovers are then used in a First-In, First-Out (FIFO) manner, meaning the oldest credits are used before any newer ones to prevent them from expiring after their 10-year limit.

Common traps and pitfalls to avoid

One of the most troubling issues arises from the interaction between the Foreign Earned Income Exclusion (FEIE) and Foreign Tax Credits. Much like attempting to cash the same check twice, seeking to claim both benefits on the same income inevitably leads to IRS problems.

Accounting for time is also another issue. Those who lose track of their 10-year carryforward windows often watch valuable credits evaporate. A $5,000 credit carried forward from 2015 becomes worthless in 2026, regardless of its potential value.

Further problems are often encountered when dealing with the IRS’s technical rules, particularly regarding income categorization and qualifying taxes. Changes in your level of involvement—for example, shifting a rental property from passive income to business income—can move the income into a different FTC “basket,” which may invalidate a carefully planned credit strategy.

Many taxpayers also mistakenly assume all foreign taxes qualify. In reality, non-income levies like VAT on purchases or property taxes on a foreign apartment don’t qualify for the credit.

Finally, a major tax planning concern is the “use-it-or-lose-it” rule upon death. Unlike many other tax benefits, accumulated foreign tax credits don’t transfer to heirs—a consideration that elderly taxpayers with substantial carryovers need to be aware of.

Strategies to maximize FTC benefits

Careful timing of income recognition can dramatically impact your credit use. A consultant with flexible billing might strategically accelerate or delay income to align tax years more favorably, maximizing credit use while minimizing carryover periods.

The choice between Foreign Tax Credit and Foreign Earned Income Exclusion is a major fork in the road. While the exclusion might offer immediate benefits, it could preclude more valuable credit opportunities down the line, especially when considering potential carryovers.

Business structures can serve as powerful tools for credit optimization. A self-employed professional might benefit from incorporating in a way that provides greater control over income timing and character, improving their ability to use credits efficiently.

Regular reviews with international tax specialists often reveal overlooked opportunities. Tax professionals can spot patterns, possibilities, and opportunities that might escape even financially experienced taxpayers, potentially identifying thousands in recoverable taxes through better credit use.

How Harness can help

At Harness, we can help you address the complexity of the Foreign Tax Credit Carryover by connecting you to international tax specialists. Our professional network provides highly personalized tax advice, delivering maximum credit use and peace of mind, especially when dealing with the IRS’s technical rules

Get started with Harness and find a dedicated specialist who can accurately manage your carryover strategy, identify any overlooked opportunities, and keep you compliant.

Disclaimer:

Tax related products and services provided through Harness Tax LLC. Harness Tax LLC is affiliated with Harness Wealth Advisers LLC, collectively referred to as “Harness Wealth”. Harness Wealth Advisers LLC is a paid promoter, internet registered investment adviser. Registration does not imply a certain level of skill or training. This article should not be considered tax or legal advice and is provided for informational purposes only. Please consult a tax and/or legal professional for advice specific to your individual circumstances. This article is a product of Harness Tax LLC.

Content was prepared by a third-party provider and not the adviser. Content should not be regarded as a complete analysis of the subjects discussed. Although we believe the content is reliable, it is not guaranteed as to accuracy and does not purport to be complete nor is it intended to be the primary basis for financial or tax decisions.